When foreign founders set up a U.S. company, compliance usually starts and ends with the business itself. Formation documents, an EIN, annual filings, maybe Form 5472 — those boxes get checked, and it feels like the job is done.

That assumption causes trouble later.

The moment money, ownership, or financial relationships exist outside the United States, the rules change. Not because tax is owed, but because the IRS wants visibility. And visibility means reporting — sometimes in places most founders don’t even know to look.

Forms 3520 and 3520-A are a common example. They don’t deal with business income in the traditional sense. Instead, they come into play when foreign trusts, overseas gifts, or inherited assets connect back to a U.S. taxpayer. Many founders trigger these filings without realizing it, often through family arrangements or structures set up long before a U.S. company ever existed.

What makes these forms particularly dangerous is how quietly problems build. There’s no automatic reminder. No withholding. No obvious red flag at the time of filing. Penalties usually appear later, after the IRS reviews past returns or matches information from other disclosures. By then, the numbers can be hard to ignore.

For foreign entrepreneurs with any U.S. tax footprint, understanding where Forms 3520 and 3520-A fit — and whether they apply at all — is less about paperwork and more about risk management. Missing them is easy. Fixing them later is not.

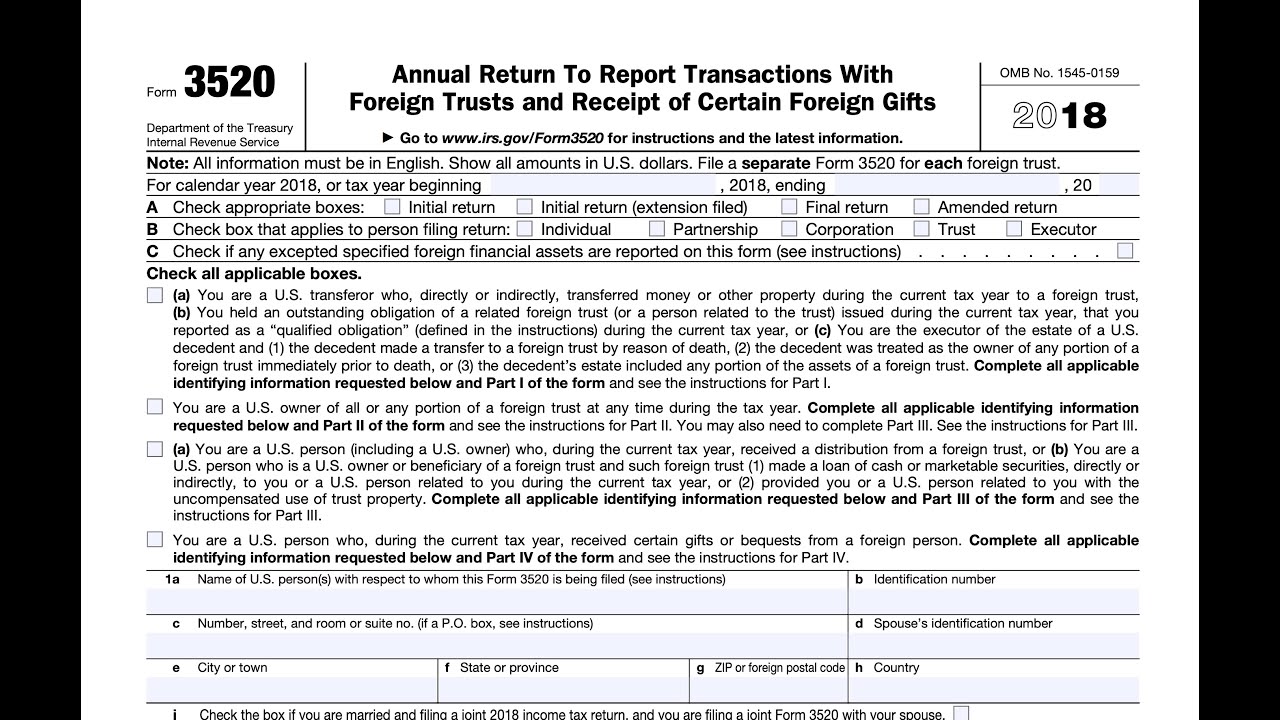

What Is Form 3520?

Form 3520 is an information return filed by individuals, not businesses. It is used to report certain transactions between a U.S. person and foreign trusts or foreign individuals.

The key point is this: Form 3520 does not calculate tax.

Its purpose is disclosure.

The IRS uses this form to track:

- Money or assets moving into the U.S. from abroad

- Foreign trust relationships

- Large foreign gifts or inheritances

Failing to file it correctly can result in penalties even if the underlying transaction was fully legal and non-taxable.

What Is Form 3520-A?

Form 3520-A comes into play when a foreign trust has a U.S. owner. It’s an annual reporting form tied to the trust itself, not the individual.

On paper, the filing responsibility belongs to the trust. In real life, that responsibility usually lands on the U.S. owner’s shoulders. If the form isn’t submitted correctly or on time, the IRS doesn’t chase the trust overseas — it looks to the U.S. person connected to it.

That’s why this form causes problems. Many owners assume it’s “not their filing” and find out years later that penalties were assessed against them personally.

Who Is Considered a “U.S. Person” for These Forms?

For Forms 3520 and 3520-A, a U.S. person includes:

- U.S. citizens.

- U.S. residents for tax purposes.

- Green card holders.

- Certain non-residents who meet the substantial presence or election rules.

Many foreign founders become U.S. persons for tax purposes without realizing it, especially after relocating, obtaining residency, or making certain elections related to their U.S. LLC.

Once classified as a U.S. person, foreign trust and gift reporting rules apply — regardless of where the trust or assets are located.

Common Situations Where Foreign Founders Trigger Form 3520

Form 3520 is required in several scenarios that frequently affect international entrepreneurs.

1. Receiving a Large Gift or Inheritance from Abroad

If a U.S. person receives:

- Gifts from a non-U.S. individual, or

- Inheritances from a foreign estate

If the total value exceeds IRS thresholds for the year, Form 3520 must be filed.

This applies even if:

- The money was transferred into a U.S. bank account.

- The funds were later invested into a U.S. LLC.

- No tax was owed on the transfer.

The IRS wants disclosure, not payment.

2. Owning or Benefiting from a Foreign Trust

Foreign trusts are common in many countries for asset protection, family planning, or investment purposes. A U.S. person may trigger Form 3520 if they:

- Created a foreign trust

- Transferred assets to a foreign trust

- Received distributions from a foreign trust

- Are treated as the owner of a foreign trust under IRS rules

This includes situations where the trust existed long before the person became a U.S. tax resident.

3. Using Foreign Trusts in Business or Investment Structures

Some foreign founders use trusts to:

- Hold shares in foreign companies

- Own intellectual property

- Manage family investments

If a U.S. person interacts with these trusts — directly or indirectly — reporting obligations may arise, even when the trust is part of a larger business structure.

When Form 3520-A Comes Into Play

Form 3520-A is required when a foreign trust is treated as having a U.S. owner under U.S. tax rules. That ownership isn’t limited to names on a trust deed. Instead, the IRS looks at how much influence or benefit a U.S. person has over the trust.

This can include the ability to control trust decisions, access to income or principal, or powers the original settlor kept after creating the trust. In many cases, people are surprised to learn they are considered an “owner” even without a formal title.

Once a U.S. owner exists, the foreign trust is expected to file Form 3520-A each year. When it isn’t filed, the IRS usually looks to the U.S. person connected to the trust — not the foreign trustee — to explain the omission and deal with any penalties. Additionally, to avoid missing other critical reporting obligations, you should understand FBAR and FATCA filing requirements for U.S. LLC owners .

Filing Deadlines You Cannot Miss

Deadlines matter because penalties start automatically.

- Form 3520

Due on the same date as the individual’s federal tax return (including extensions). - Form 3520-A

Due March 15 each year.

Extensions must be requested separately and on time.

Missing Form 3520-A is one of the fastest ways to trigger large IRS penalties.

Penalties: Why These Forms Matter So Much

The penalty structure for Forms 3520 and 3520-A is severe compared to most other information returns.

Common penalties include:

- A percentage of the value of unreported gifts or distributions

- Penalties tied to the trust’s asset value

- Ongoing monthly penalties until the form is filed

- Additional penalties if the IRS determines the failure was willful

These penalties apply even when no tax is owed.

For foreign founders, this is often the most surprising part of the process.

How Forms 3520 and 3520-A Interact with Other Filings

These forms do not exist in isolation. They often overlap with:

- FBAR (FinCEN Form 114)

- FATCA (Form 8938)

- Form 5471 or 5472

- Individual income tax returns

Each form has its own rules. Filing one does not replace another.

A common mistake is assuming that reporting a foreign account or asset elsewhere covers trust or gift reporting. It does not.

Practical Compliance Tips for Foreign Founders

In 2026, staying compliant requires planning, not guesswork.

Foreign entrepreneurs should:

- Review ownership and control over any foreign trusts annually.

- Track gifts and inheritances received from abroad.

- Coordinate trust reporting with personal tax filings.

- Address missed filings early rather than waiting for IRS notices.

- Work with advisors familiar with cross-border trust rules.

These steps reduce exposure and help avoid penalties that are difficult to reverse. If you hold foreign financial accounts, it’s also important to compare FBAR and IRS reporting thresholds for foreign accounts.

Final Thoughts

Forms 3520 and 3520-A are not commonly discussed, but they carry outsized risk for foreign founders with U.S. tax exposure.

They do not determine how much tax you owe. They determine whether the IRS knows about certain foreign relationships and transfers. That distinction is why so many penalties arise — not from wrongdoing, but from missing disclosures.

If you operate internationally, have family assets abroad, or use trusts as part of your planning, these forms deserve attention long before a filing deadline approaches. Addressing them early is far easier than fixing them after the IRS comes knocking. For a broader overview of compliance requirements and business filing essentials for international founders, be sure to learn more about U.S. compliance requirements for foreign founders here — Filing Express.

FAQs

1. If my parents sent me money from abroad, do I need to file Form 3520?

Sometimes, yes. If you’re treated as a U.S. taxpayer and the total amount you received goes beyond the IRS reporting threshold, the transfer has to be disclosed — even though it was a family gift and not income.

2. Does filing Form 3520 automatically create a tax bill?

No. Filing the form doesn’t turn a gift or inheritance into taxable income. Its purpose is reporting, not collecting taxes. Many people file it simply to document where the funds came from.

3. What if the foreign trust doesn’t file Form 3520-A?

That usually doesn’t end the issue. When a foreign trust fails to file, responsibility often shifts to the U.S. person connected to it, along with the potential penalties.

4. I missed these filings in previous years. Is it too late to fix?

No, but delays make things harder. Voluntarily correcting past filings is almost always viewed more favorably than waiting for the IRS to raise the issue.